There is a version of running a business where you check the bank balance every morning and make decisions from there. If the number looks okay, the day feels okay. However, if it looks low, there is a quiet panic that follows you into every meeting.

Most business owners have lived some version of that. Moreover, most of them know, somewhere in the back of their mind, that a bank balance is not actually a financial plan.

A 13-week cash flow analysis is one of the most practical tools for getting out of that cycle. It is not complicated. It does not require sophisticated software or a finance team. But it does require knowing your numbers — and being honest about what they are telling you.

Here is what it is, how it works, and how to know whether your business needs one right now.

What a 13-Week Cash Flow Analysis Actually Is

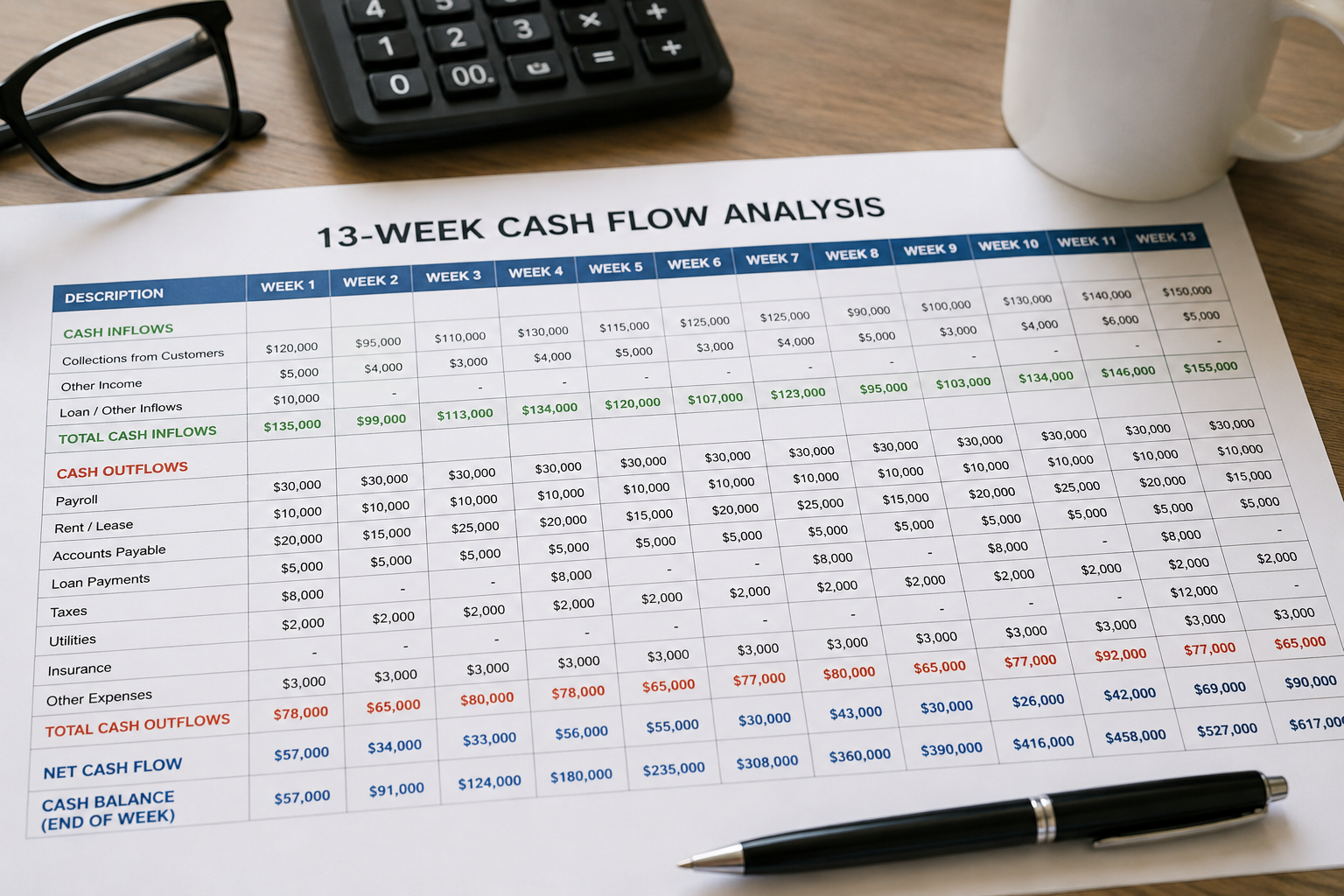

A 13-week cash flow analysis is a rolling, week-by-week projection of every dollar expected to come into and go out of your business over the next 13 weeks. That period is roughly one quarter.

That is it. Inflows and outflows, mapped out by week, for 90 days.

The reason 13 weeks became the standard is practical. It is short enough to be specific and reasonably accurate. Also, it is long enough to surface problems before they become crises. A 12-month cash flow projection has its place in strategic planning. However, the further out you project, the more assumptions you are stacking on top of each other. Instead, a 13-week model keeps you close enough to reality to act on what you see.

This is a tool originally associated with distressed businesses and restructuring situations — lenders and turnaround advisors often require them when a company is under financial stress. But that framing undersells it. In fact, a 13-week cash flow analysis is genuinely useful for any business going through a period of growth, uncertainty, or transition — not just ones in trouble.

What Goes Into It

The model is built in three parts.

Cash inflows are every source of cash expected to arrive in the business over the 13-week period. For most businesses, this is primarily collections from customers or clients — but the timing matters enormously. Revenue recognized on an invoice is not the same as cash in the bank. For example, if you invoice on net-30 terms, the cash from a sale made this week does not show up for another month. Therefore, the model has to reflect when cash actually lands, not when the sale happens.

Other inflows might include owner contributions, loan proceeds, asset sales, or tax refunds — anything that puts cash into the business regardless of whether it shows up on your income statement.

Cash outflows are every obligation the business has to pay over the same period. This includes payroll, rent, vendor payments, loan principal and interest, taxes, insurance, software subscriptions, and owner draws. Every recurring and known one-time expense gets mapped to the week it is due.

This is where a lot of business owners have a reckoning. When you lay out every outflow by the week it hits, you start to see the shape of your cash requirements in a way that a monthly income statement never shows you. For instance, two weeks with payroll landing the same week as a large vendor payment and a quarterly insurance premium can look fine on a P&L. However, it can feel catastrophic on a Tuesday.

Net cash position is the result — what you expect to have at the end of each week after accounting for that week’s inflows and outflows. Negative weeks are not automatically a crisis, but they require a plan. You need to know in advance which weeks are tight, not discover it when the payment is due.

Why It Is Different From Your P&L and Balance Sheet

Your profit and loss statement tells you how the business performed over a period of time. It is structured around revenue and expenses — not cash. In contrast, a business can show a healthy net profit and still be technically insolvent if cash is not collected on time and obligations are due now.

Your balance sheet gives you a snapshot of your financial position at a point in time. It tells you what you own and what you owe. However, it does not tell you when cash arrives or when payments are due.

The 13-week cash flow model is the only one of the three that shows you the timing. And timing is what keeps a business operational. You do not need to be profitable every single week to stay in business. However, you do need enough cash on hand every single week to meet your obligations.

This is also why knowing the difference between profit and cash is one of the most important concepts for business owners to genuinely internalize. The 13-week model makes that distinction impossible to ignore.

When a 13-Week Cash Flow Analysis Is Most Valuable

During periods of rapid growth. Growth consumes cash in ways that catch business owners off guard. For example, you are hiring ahead of revenue, buying inventory before you collect, and extending credit to new customers. More revenue does not mean more cash — often it means less, at least in the short term. In fact, a 13-week model shows you where the gaps will be before they arrive.

When revenue is seasonal or uneven. If your business has predictable slow periods — a construction company in winter, a tax firm outside of filing season, a retailer between holidays — a 13-week model helps you plan across the gap. You can see exactly how many weeks you need to fund from reserves. Furthermore, you can determine whether you have enough to do it.

Before taking on new debt. Before you apply for a loan or a line of credit, a 13-week cash flow model helps you understand what you actually need, when you need it, and how repayment will affect your ongoing cash position. It is exactly the kind of analysis that makes a lending conversation more credible. This is because you are showing a lender that you understand your own cash dynamics, not just your account balance.

When the business is under pressure. A slow quarter, a large client who went quiet, a key employee who left unexpectedly — these create uncertainty. The 13-week model does not eliminate that uncertainty, but it gives you a clear picture of how long your runway is. It also shows what decisions you need to make to protect it.

When you are preparing for a transaction. Whether you are acquiring another business, bringing in a partner, or exploring a sale, buyers and investors want to understand your cash position and your cash generation ability. A well-constructed 13-week model demonstrates financial fluency. Additionally, it gives any counterparty confidence in what they are looking at.

How to Build One

You do not need specialized software to build a 13-week cash flow model. A well-structured spreadsheet works. What you do need is accurate, current bookkeeping — because the model is only as reliable as the data that goes into it.

Start with your current cash balance. That is week zero.

Map out your expected inflows week by week. Pull from your accounts receivable aging report to understand when outstanding invoices are likely to be collected. Then layer in any other expected cash receipts and be honest about the timing — conservative is better than optimistic here.

Map out your expected outflows week by week. Pull your recurring obligations from your books. Next, add in known one-time payments. Do not forget quarterly or annual expenses that might fall within the 13-week window — insurance renewals, estimated tax payments, equipment maintenance, and so on.

Calculate your net cash position at the end of each week. Look for the weeks where cash goes negative or drops below your minimum comfortable operating level. Those are the weeks that need a plan.

Then update it. The model is most useful when it is a living document — updated weekly as actual results come in and projections are adjusted. Furthermore, the variance between what you projected and what actually happened is information. Over time, it makes your projections more accurate and your financial intuition sharper.

What It Tells You That Nothing Else Does

The 13-week cash flow model answers a question that business owners ask themselves constantly but rarely have a clear answer to: how long can we sustain current operations if nothing changes?

It also answers the next set of questions that follow from that one. In the event a slow period hits, which weeks are vulnerable? If we bring on that new hire, when does the payroll impact start and how does it stack against our expected inflows? If we take on that large project, does it help or hurt our cash position in the short term given the upfront costs?

When your financials are organized and current, building a 13-week model is a natural next step. It takes the accuracy of your bookkeeping and turns it into forward-looking clarity — which is exactly what fractional CFO work is designed to do.

You stop managing by the bank balance. Instead, you start managing by the plan.

Does Your Business Need One Right Now?

If any of the following are true, the answer is probably yes.

You have had at least one moment in the past year where you were not sure if payroll would clear. Maybe you have a slow season coming and you are not sure your reserves will cover it. Or you are growing and it does not feel as good as it should because cash is still tight. You are about to take on significant new debt or a major new contract. Furthermore, you have been telling yourself you need to get more disciplined about cash flow but have not built anything systematic yet.

You do not need a financial crisis to justify building a 13-week cash flow model. You just need to care about running your business with clarity instead of guesswork.

If you are not sure where to start or whether your books are in a place where this kind of analysis is even possible right now, let’s talk. That is exactly the kind of conversation we have with business owners every day.

Because the bank balance will tell you where you are today. Your 13-week model tells you where you are going.

Leave a Reply